Quarterly Money Market Commentary

June 30, 2025

First American Money Market Funds

What market conditions had a direct impact on the bond market this quarter?

Economic Activity – U.S. economic growth during the second quarter of 2025 (Q2) was characterized by slower activity and growing uncertainty as the economy reacted to the volatile rollout of trade tariffs and rising geopolitical tensions. U.S. Gross Domestic Product (GDP) is projected to grow near 2.0% for Q2. This follows a 0.5% contraction in the first quarter due to one-off trade deficit effects. Growth is projected to slow over the remainder of the year, however, as persistent trade policy uncertainty and expectations for higher inflation drive cautious behavior from consumers and businesses. Personal consumption slowed during the quarter, reflecting declining confidence and payback from earlier tariff front-running. Labor markets remained resilient with solid hiring activity and low layoffs, but cracks in underlying data are starting to show including rising continuing jobless claims, slowing wage growth, and reduced breadth of hiring. Month-to-month U.S. job openings continue to be volatile with May openings rising to 7.8 million open positions while the total number of unemployed workers in the labor force as of June remained stable at 7.0 million. Monthly Nonfarm Payrolls (NFP) growth remains healthy, averaging 150,000 during Q2 and the U3 Unemployment Rate was 4.1% in June. Average Hourly Earnings growth slowed to 3.7% year-over-year (YoY) but continues to be above pre-pandemic levels. U.S. inflation readings remained above the Federal Reserve’s (Fed) 2% target in Q2 with the Consumer Price Index (CPI) stable at 2.4% in May as lower energy prices offset modest increases in food and core services prices. Core inflation was also stable with CPI ex. food and energy rising 2.8% YoY for May and the Fed’s preferred inflation index – the PCE Core Deflator Index – increasing 2.7% YoY. Excess inventories and softer demand have thus far limited upward price pressures, but inflation is projected to increase in the second half of the year as tariff-related costs begin to emerge. However, the timing, extent, and duration of these pressures are unknown.

Monetary Policy – The Fed left its federal funds target range unchanged during the quarter at 4.25% to 4.50%. The Fed’s post-meeting statement was little changed while noting uncertainty has “diminished but remains elevated.” With current policy well-positioned to respond to material changes in the outlook, Fed Chair Powell continues to stress patience as the Committee awaits more clarity surrounding the impact tariffs will have on growth and inflation. Additionally, the Fed maintained the pace of its balance sheet reduction program (quantitative tightening) with a monthly cap on Treasury securities of $5 billion and on agency mortgage-backed securities of $35 billion.

The Federal Open Market Committee (FOMC) released its updated Summary of Economic Projections at the June meeting. The FOMC’s “dot plot” continues to suggest 50 basis points (bps) in rate cuts by the end of 2025 (target range of 3.75% to 4.0%), although there is a divergence of views as eight members are calling for two rate cuts in 2025 and seven are calling for none. The median dots show further rate cuts of 25 bps in 2026 (previously 50 bps) and 25 bps in 2027 (unchanged), and the estimated longer-run neutral rate was unchanged at 3.0%. The FOMC’s economic projections were revised to show higher expected core inflation and a higher unemployment rate in 2025-2027 with a lower GDP growth forecast for 2025-2026 compared to the prior release.

Fiscal Policy – The whirlwind of fiscal policy action beginning in Q1 extended through Q2, with the quarter starting with a steady stream of tariff announcements and closing with the passage of the sweeping One Big Beautiful Bill Act. The Trump Administration’s “Liberation Day” tariff announcement on April 2 included a baseline 10% tariff on all imports and “reciprocal” tariffs on dozens of countries that have trade deficits with U.S. Reciprocal tariffs were paused for 90 days (deadline subsequently extended to August 1) as the Administration continues to work on individual trade deals. As of this writing, the U.K. and Vietnam are the only countries with trade deals in place. Additional tariffs have also been placed on steel and aluminum, automotives, and non-USMCA-compliant goods from Canada and Mexico and further sectoral tariffs are expected over the near-term including semiconductor chips and pharmaceuticals. The tariff situation remains fluid, but implementation of expansive tariff policies will serve as an economic headwind moving forward.

The other fiscal highlight was passage of the One Big Beautiful Bill Act on July 4. Among other things, the Act permanently extends the 2017 tax cuts, boosts spending for defense, immigration, and border control, and raises the debt limit by $5 trillion. The Act also includes spending cuts to Medicaid and clean-energy tax credits and subsidies. Passage of the Act should provide a modest boost to economic growth next year and removes debt ceiling risk for a couple of years. After addressing the debt ceiling and renewing the 2017 tax cuts, Congress’ remaining key deadline for the year will be to pass a government funding bill by September 30. On the municipal front, the sector is facing growing headwinds to finances including rising demand for local funding, evaporation of Federal covid money, and unknown impacts from tariffs on economic activity. Fortunately, municipal revenues have remained solid to this point and reserves remain strong.

Credit Markets – The second quarter got off to a rocky start on the heels of the Trump Administration’s Liberation Day tariff announcement on April 2. Credit spreads widened and treasury yields fell in reaction to the more severe than expected proposals. Further uncertainty was introduced when Israel attacked Iranian nuclear capabilities, sending oil prices higher and creating concerns over a potential wider regional conflict. Credit markets and spreads recovered from their peaks as the Trump administration paused the implementation of certain tariffs until July 9 and new trade deals were negotiated, easing concerns over worst-case economic scenarios. While new issuance was restrained in the first part of the quarter, fixed income markets for the most part continued to function properly with solid liquidity and no meaningful deterioration in the credit quality of held positions.

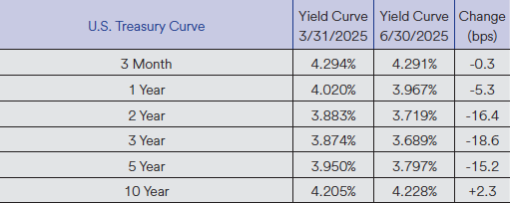

Yield Curve Shift

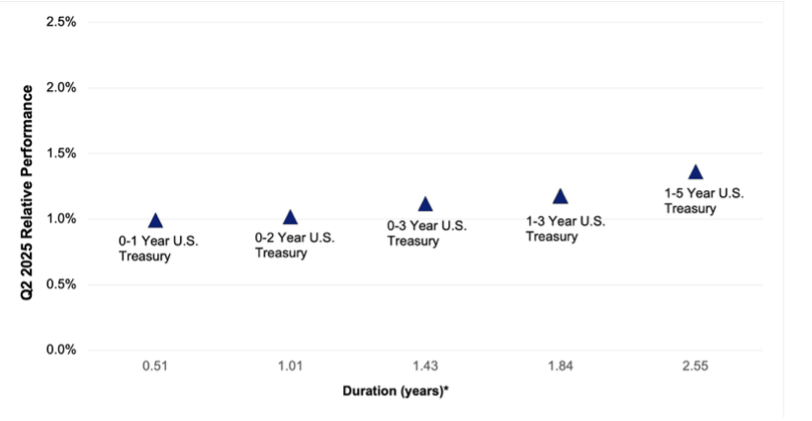

Duration Relative Performance

*Duration estimate is as of 6/30/2025

Falling yields contributed to the quarter’s strong fixed income returns. The three-month to 10-year portion remained inverted, with front-end yields remaining stable on no Fed policy changes in the quarter and 10-year yields only rising 2.3 bps. With two to five-year yields falling more than short-term yields, longer duration strategies outperformed short duration strategies. There was some volatility along the front-end of the yield curve, with two-year yields trading within a range of 3.60% and 4.05% in the quarter, presenting some tactical opportunities to position portfolio duration.

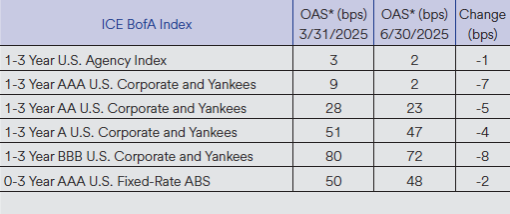

Credit Spread Changes

Corporate credit spreads tightened in the quarter, more than recovering from the April 2 tariff announcement-induced spread widening. Credit spreads are relatively tight from a historical basis. Spread performance in the ABS sector was more muted than in the corporate sector, leading to underperformance versus investment-grade corporates.

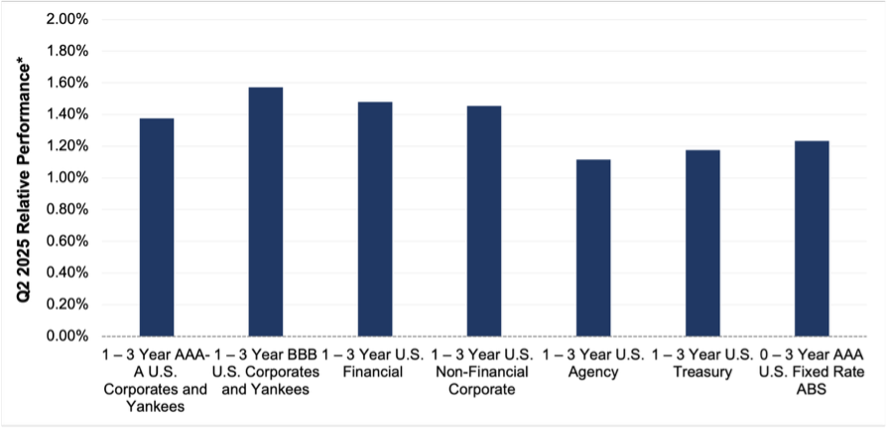

Credit Sector Relative Performance of ICE BofA Indexes

*Data is as of 6/30/2025

Declining treasury yield curve levels and tightening credit spreads across the investment-grade universe generated strong absolute performance for all fixed income sectors. Down-in-credit outperforming higher-rated credit was a general theme, highlighted by the BBB corporate index’s 19.6 bps outperformance of the AAA-A corporate index.

What were the major factors influencing money market funds this quarter?

The second quarter of 2025 saw the Fed continue to hold rates in the 4.25-4.50% range, putting themselves in a “wait and see” mode after the “Liberation Day” tariff announcements. With inflation above Fed targets, but showing signs of abating, labor and economic data solid, but softening, market expectations for the Fed moved a bit dovish, indicating two-three 25 bps cuts by year end. There are varying opinions on the timing and pace of future rate activity and ultimately the Fed has stated it will remain data dependent, so no clear path has been determined. The challenge for managers going forward will be determining how the economic, inflation and employment data will influence FOMC action. Industry wide, money market fund assets trended higher during the quarter as short-term yields continue to attract investors. Money market funds remain a viable option relative to other short-term cash equivalent options.

First American Prime Obligations Funds

Credit conditions and trading ranges have been stable given the current rate, geopolitical and economic environment. Considering the yield curve and a conservative cash flow approach, the First American Funds were positioned with strong portfolio liquidity metrics influenced by fund shareholder makeup. We continued to employ a heightened credit outlook, maintaining positions presenting minimal credit and headline risk to the Fund’s investors. During the first quarter, our main investment objective was to prioritize liquidity while opportunistically enhancing portfolio yield, with a combination of fixed and floating rate securities, reflecting our economic, credit and interest rate outlook. We believe the credit environment and higher relative fund yields make the sector an appropriate short-term option for investors.

First American Government and Treasury Funds

As the Fed maintains a more cautious approach, money market funds remained defensive, positioning to preserve yields with the potential for falling rates. Managers extended durations, investing in longer-term securities to get ahead of a forecasted lower yield environment. These market dynamics support a more barbell investment strategy. For money market fund investors, extension into lower yielding long-term securities puts marginal downward pressure on portfolio yields. However, the slowing pace of Fed activity and relatively flat yield curve should mute the downward pressure on front-end rates and ultimately should slow the decline in money market fund yields, until the Fed’s next moves become clear. Strategically, when presented with appropriate value, managers purchased floating-rate investments anticipated to benefit shareholders over the securities holding period. Investment strategy will be fluid in the coming quarters as markets make determinations on the Fed’s comfort level with inflation, economic growth and ultimately the timing and pace of future Fed policy action.

First American Retail Tax Free Obligations Fund

Individual income tax payments pushed tax-exempt money market fund yields sharply higher in April. Concurrently, the tariff announcements and economic uncertainty rippled thru financial markets and led municipal investors to raise cash and build liquidity. SIFMA, an index comprised of 7-day variable rate demand notes, reached a high of 4.41%. And yields for municipal notes, with one-year maturities, jumped 35-45 bps. Later in the quarter, rates reversed lower due to better reinvestment demand from municipal bond maturities and coupon payments and some de-escalation in trade policy. Positioning continues to emphasize higher allocations to fixed-rate securities and longer weighted average maturities versus competitor averages. This strategy is cognizant of both the strong technicals in the municipal market during July and August and the potential for eventual interest rate cuts from the Federal Reserve later this year.

What near-term considerations will affect fund management?

Industry-wide, we anticipate that prime fund yields will gradually decline as managers roll maturities into lower-yielding securities that are pricing in future rate cuts. However, broadly speaking, front-end yields in credit securities should continue to benefit from the overall supply of treasury securities and higher secured overnight financing rate levels. Modest spread widening, as well the impacts of a smaller prime money market fund universe should create competition among credit issuers for the marginal dollar and support yields. In the coming quarters, we will seek to capitalize on investment opportunities that make economic sense based on market outlooks and break-even analysis. The Institutional and Retail Prime Obligations Funds should remain reasonable short-term investment options for investors seeking higher yields on cash positions while assuming minimal credit risk.

Yields in the government-sponsored enterprise (GSE) and Treasury space will decline in concert with anticipated and realized Fed rate cuts. As with non-government debt, Government and Treasury fund yields will continue to gradually decline as managers roll maturities into securities with lower yields pricing in future rate reductions. Managers will defend against future cuts by extending to optimal spots on the curve relative to Fed rate forecasts, policy impacts and market volatility. We anticipate some moderate yield dislocations in Treasury, GSE and Repo issues as Treasury supply fluctuates. It’s worth noting that the extension of the debt ceiling has ended extraordinary measures and we expect an acceleration in T-Bill supply to replenish the Treasurys General Account. In general, in the short term, we expect T-Bill and Repo levels to rise, giving a boost to money market fund-yields until the new supply is evenly absorbed into the market. Going forward, management will exploit large supply changes in Treasury issuance that create volatility and yield opportunities on the front end as the forces of supply and demand seek optimization. Fund management will continue to seek value in all asset classes and exploit market conditions that support domestic and global economic outlooks.

For more information about the portfolio holdings, please visit

https://www.firstamericanfunds.com/index/FundPerformance/PortfolioHoldings.html

Sources

Bloomberg

https://www.federalreserve.gov/monetarypolicy/files/monetary20250507a1.pdf

https://www.federalreserve.gov/monetarypolicy/files/monetary20250618a1.pdf

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20250618.pdf

https://economics.bmo.com/en/publications/detail/56a75a45-fbc2-49b6-9fd3-0fd5426af907/

https://www.npr.org/2025/07/09/nx-s1-5460936/trump-tariffs-economy-china-policy