Quarterly Money Market Commentary

December 31, 2025

First American Money Market Funds

What market conditions had a direct impact on the bond market this quarter?

Economic Activity – The U.S. economy entered the fourth quarter of 2025 (Q4) in a strong position, with third quarter growth exceeding expectations on solid consumer spending and AI-driven business investment. However, economic activity in Q4 was disrupted by the federal government shutdown and its effects on data availability, creating uncertainty for much of the quarter. U.S. Gross Domestic Product (GDP) growth is projected to slow toward 1.5% in Q4, but negative effects from the shutdown should prove temporary and be recouped throughout the first quarter of 2026. Consumer confidence weakened amid shutdown concerns and labor market pessimism, particularly among lower-income households. Despite this decline in sentiment, consumer spending remained resilient through the holiday season, highlighting the ongoing disconnect between sentiment and actual activity. Employment conditions continued to cool, reflecting weak labor demand as businesses maintained a low-hire/low-fire strategy. U.S. job openings remained volatile month to month, yet the broader downward trend persisted in Q4, with November openings at 7.1 million versus 7.5 million total unemployed workers in December. Monthly Nonfarm Payrolls (NFP) growth remained subdued, averaging 14,500 in the second half of 2025, and overall payrolls contracted in Q4 due to federal workforce reductions. The unemployment rate held at 4.4%, supported by low layoffs and slower labor force growth. Average hourly earnings continued to show strength, rising 3.8% year-over-year (YoY) in December. Inflation eased, with headline Consumer Price Index (CPI) declining to 2.7% in December and core CPI (excluding food and energy) rising 2.6% YoY for December. However, data disruptions from the shutdown raise accuracy concerns. Confirmation is needed to validate disinflation, as tariffs and expansionary fiscal policy pose upside risks, making near-term progress toward the Fed’s 2% target unlikely.

Monetary Policy – TThe Fed continued its easing cycle in Q4, lowering the federal funds target range by 25 basis points (bps) in both October and December, ending the year at 3.50% to 3.75%. The December decision drew three dissents—the most since 2019. Kansas City Fed President Schmid and Chicago Fed President Goolsbee favored no change to the target range, while Governor Miran preferred a 50 bps reduction. The Fed revised its December post-meeting statement to note that “the extent and timing of additional adjustments” will depend on the incoming data and economic outlook. This change in language suggests a more patient approach to easing, with consensus expectations pointing to a pause at the upcoming January meeting. Additionally, the Fed announced plans to begin reserve management purchases (RMPs) of Treasury bills to maintain reserves at an “ample level.” Initial RMPs are expected to total approximately $40 billion per month, tapering to $20-$25 billion per month over time.

The December Summary of Economic Projections kept the “dot plot” unchanged, showing 25 bps cuts in 2026 and 2027. However, individual projections remain widely dispersed, underscoring division among Federal Open Market Committee (FOMC) members regarding the future path of policy rates. The estimated longer-run neutral rate was unchanged at 3.0%. Median forecasts now call for stronger GDP growth, lower inflation, and reduced unemployment—assumptions that appear inconsistent with labor market risks and a lower rate outlook.

Fiscal Policy – Fiscal policy remained expansionary in the fourth quarter, despite the quarter beginning with the longest government shutdown in U.S. history (43 days). Legislative measures and government spending continued to support growth, including passage of the One, Big, Beautiful Bill (OBBB) Act earlier in the year. Among other provisions, the Act permanently extends the 2017 tax cuts, increases defense spending, and introduces growth-friendly measures such as immediate deduction of capital expenses for businesses—steps expected to boost investment and provide an economic tailwind. Legislation to end the shutdown included a continuing resolution to fund the government at current levels through January 2026, while providing full-year funding for the Agriculture Department, military construction, and the legislative branch.

Looking ahead to the upcoming midterm elections, we anticipate additional accommodative fiscal policy measures in 2026. However, the landscape is not without challenges, including legal questions surrounding tariffs imposed under the International Emergency Economic Powers Act (IEEPA) and the risk of another government shutdown. In November, the U.S. Supreme Court heard oral arguments on the Administration’s use of IEEPA to implement tariffs. While legal experts predict a ruling against the Administration, tariffs are likely to remain in some form given their prominence in the Administration’s agenda. Additionally, the funding deal that reopened the government in November expires at the end of January, leaving Congress less than one month to pass spending legislation or risk another shutdown. On the municipal front, the sector faces growing financial pressures from increased local funding needs, the exhaustion of federal pandemic aid, and economic uncertainties related to tariffs. Municipalities enter this period from a position of relative strength, however, as solid revenues and robust reserves provide the flexibility needed to navigate these headwinds.

Credit Markets – Financial markets navigated several headwinds in the fourth quarter, including persistent inflationary pressures, weakening labor market data, and the longest government shutdown in U.S. history, lasting 43 days. Despite these challenges—and already stretched valuations—risk assets remained resilient. Multiple Federal Reserve rate cuts, along with generally positive expectations for economic growth in 2026, supported investor sentiment.

Investment-grade credit spreads experienced only modest widening and remained near multi-year lows. The pace of new investment-grade corporate bond issuance slowed somewhat during the quarter following a particularly strong September. Supply continues to be well received, secondary market liquidity remains solid, and there was no meaningful deterioration in the credit quality of held positions..

Yield Curve Shift

|

U.S. Treasury Curve |

Yield Curve 9/30/2025 |

Yield Curve 12/31/2025 |

Change (bps) |

|---|---|---|---|

|

3 Month |

3.932% |

3.633% |

-29.9 |

|

1 Year |

3.614% |

3.475% |

-13.9 |

|

2 Year |

3.608% |

3.475% |

-13.3 |

|

3 Year |

3.619% |

3.540% |

-7.9 |

|

5 Year |

3.741% |

3.726% |

-1.5 |

|

10 Year |

4.150% |

4.169% |

1.9 |

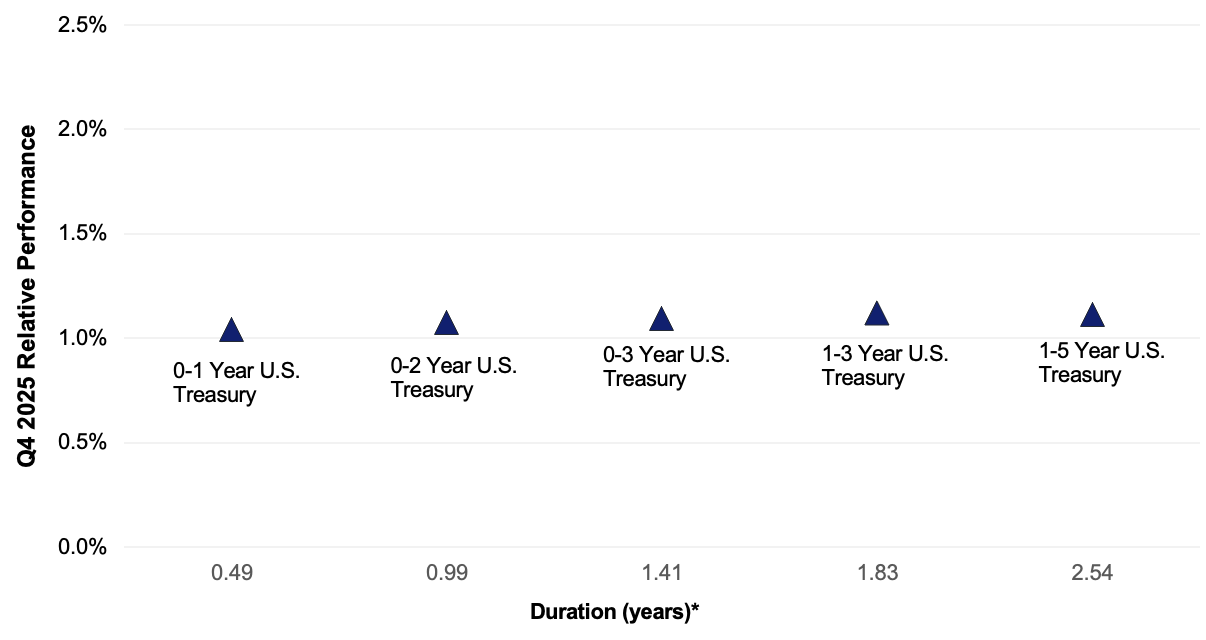

Duration Relative Performance

*Duration estimate is as of 12/31/2025

Duration positioning, like the third quarter, did not meaningfully influence the performance of short duration mandates. Treasury indices with durations ranging from 0.5 to 2.5 years delivered returns within a narrow range over the period. Yields on front end maturities (1–3 years) declined as markets priced in additional Federal Reserve rate cuts, while yields in the intermediate segment of the curve (5–10 years) remained relatively stable. This steepening bias is expected to continue through 2026 based on current consensus forecasts. However, the anticipated shifts are projected to be more muted than the approximately 40 bps move between the 2 year and 10 year segments observed in 2025.

Credit Spread Changes

|

ICE BofA Index |

OAS* (bps) 9/30/2025 |

OAS* (bps) 12/31/2025 |

Change (bps) |

|---|---|---|---|

|

1-3 Year U.S. Agency Index |

1 |

1 |

0 |

|

1-3 Year AAA U.S. Corporate and Yankees |

5 |

7 |

2 |

|

1-3 Year AA U.S. Corporate and Yankees |

23 |

25 |

2 |

|

1-3 Year A U.S. Corporate and Yankees |

40 |

44 |

4 |

|

1-3 Year BBB U.S. Corporate and Yankees |

66 |

71 |

5 |

|

0-3 Year AAA U.S. Fixed-Rate ABS |

41 |

50 |

9 |

Option-Adjusted Spread (OAS) measures the spread of a fixed-income instrument against the risk-free rate of return. U.S. Treasury securities generally represent the risk-free rate.

Investment-grade corporate credit spreads experienced only modest widening in Q4 and remained near multi year lows. These levels reflect strong corporate fundamentals and a constructive outlook for economic activity heading into 2026. Supply is expected to be elevated over the coming year, with some strategists projecting more than $2 trillion in new issuance. This could create periods of short term pressure but may also lead to more attractive valuations.

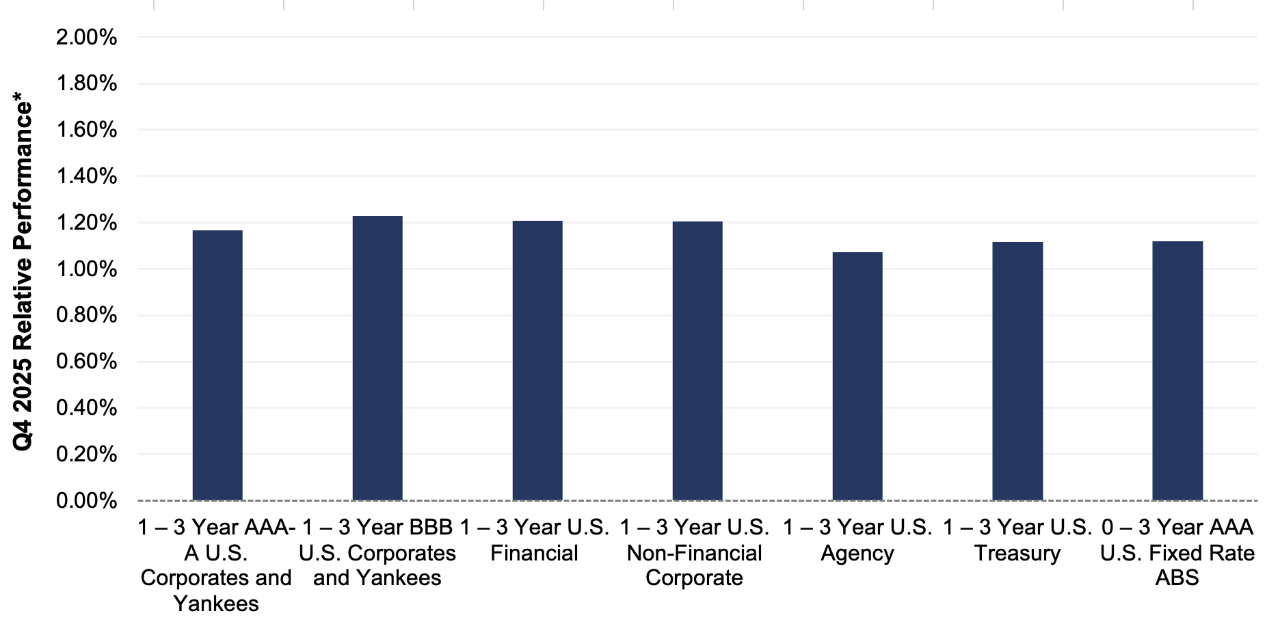

Credit Sector Relative Performance of ICE BofA Indexes

ICE BofA Index

*AAA-A Corporate index outperformed the Treasury index by 4.9 bps.

*AAA-A Corporate index underperformed the BBB Corporate index by 6.2 bps

*U.S. Financials outperformed U.S. Non-Financials by 0.4 bps

Credit portfolios continued to outperform Treasurys, despite the modest widening noted earlier. This outperformance primarily reflects the additional spread and income advantages associated with corporate securities. Although lower-rated investments delivered slightly stronger returns again this quarter, the incremental benefit is not particularly compelling on a risk adjusted basis.

What were the major factors influencing money market funds this quarter?

The fourth quarter of 2025 saw the Fed continue its easing cycle, reducing the federal funds target by 25 bps to a range of 3.50-3.75%. While inflation remains above the Fed’s preferred targets, expected labor market softening is guiding markets to price in two additional 25 bps cuts in 2026. Although there are varying opinions on the timing and pace of future FOMC actions, market consensus suggests the path forward points to lower rates. The challenge for managers will be determining how the economic, inflation, and employment data will influence the pace and timing of the easing cycle.

Industry-wide, money market fund assets continued to trend higher during the quarter, as these products remained an attractive option relative to other short-term cash equivalent options.

First American Prime Obligations Funds

Credit conditions and trading ranges have remained stable despite the current rate, geopolitical and economic environment. Considering the yield curve and a conservative cash flow approach, the First American Funds were positioned with strong portfolio liquidity metrics influenced by shareholder composition. We maintained a heightened credit outlook, prioritizing positions that present minimal credit and headline risk to investors. During the fourth quarter, our primary investment objective was to preserve liquidity while opportunistically enhancing portfolio yield through a combination of fixed- and floating-rate securities, reflecting our economic, credit and interest rate outlook. We believe the credit environment and higher relative fund yields make this sector an appropriate short-term option for investors.

First American Government and Treasury Funds

While the FOMC is somewhat divided on the need and pace of future rate cuts, the current administration appears committed to lower rates. As a result, Government Money Market Funds maintained a defensive posture, positioning to preserve yields amid expectations of falling rates in 2026. Managers extended durations, investing in longer-term securities to prepare for a forecasted lower-yield environment. These market dynamics support a barbell investment strategy. For money market funds investors, extending into lower-yielding long-term securities exerts marginal downward pressure on portfolio yields. Notably, with the end of quantitative tightening (QT) at the December Fed meeting, a more normalized Repo/SOFR rate environment is expected, which will reduce some benefits of the barbell strategy. Strategically, managers purchased floating-rate investments when appropriate value was available, anticipating benefits over the securities’ holding period. Investment strategy will remain focused on the pace of falling rates as markets assess the Fed’s comfort level with inflation, unemployment, and economic growth—all of which will influence future policy timing.

First American Retail Tax Free Obligations Fund

Municipal market conditions—particularly the periodic imbalances between reinvestment demand and supply—remain the primary factor influencing tax-free money market rates. Notably, during a period when the Federal Reserve lowered interest rates by 50 bps, SIFMA increased by an average of nearly 35 bps compared to Q3. This movement is best viewed as a “normalization” of variable-rate demand note resets following the stronger technicals experienced during the summer months. SIFMA spiked above 3% in mid-December, reflecting broker-dealer reluctance to carry inventory over year-end. These are short-term fluctuations, and we continue to position the Fund to mitigate the impact of lower resets anticipated in early 2026.

What near-term considerations will affect fund management?

Industry-wide, it is anticipated that prime fund yields will continue to gradually decline as managers roll maturities into lower-yielding securities that price in future rate cuts. However, front-end yields in corporate securities should continue to benefit from ample supply. A modest term risk premium, combined with the impacts of a smaller prime money market fund universe —which should create competition among credit issuers for marginal dollars—will also help support higher prime fund yields. In the coming quarters, we will capitalize on investment opportunities that make economic sense based on market outlooks and break-even analysis. The Institutional and Retail Prime Obligations Funds should remain reasonable short-term investment options for investors seeking higher yields on cash positions while assuming minimal credit risk.

Yields in the government-sponsored enterprise (GSE) and Treasury space will decline in line with anticipated and realized Fed rate cuts. As with non-government debt, Government and Treasury fund yields will continue to gradually decline as managers roll maturities into fixed-rate securities with lower yields that price in future rate reductions. Managers will defend against future cuts by extending to optimal spots on the curve relative to Fed rate forecasts, policy impacts, and market volatility. While debt supply remains elevated, the end of QT should normalize SOFR/Repo levels, exerting marginal downward pressure on money market fund yields. Additionally, management will exploit large supply changes in Treasury issuance that create volatility and present yield opportunities on the front end as supply and demand forces seek equilibrium. Floating-rate securities will remain a core component of the overall investment strategy, adding incremental yield and price stability..

Sources

Bloomberg

https://www.federalreserve.gov/monetarypolicy/files/monetary20251210a1.pdf

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20251210.pdf

https://www.wsj.com/politics/policy/house-spending-bill-government-shutdown-05bf3a6e?mod=hp_lead_pos2

https://www.cnbc.com/2026/01/09/trump-will-use-other-tariff-authorities-to-get-to-same-place-if-supreme-court-rules-against-him-hassett.html

Jim Palmer, CFA

Jeff Plotnik

Mike Welle, CFA